00017531622023FYFALSE30100017531622023-01-012023-12-3100017531622023-06-30iso4217:USD00017531622024-03-19xbrli:shares00017531622023-12-3100017531622022-12-31iso4217:USDxbrli:shares0001753162us-gaap:ManagementServiceIncentiveMember2023-01-012023-12-310001753162us-gaap:ManagementServiceIncentiveMember2022-01-012022-12-310001753162us-gaap:ProductAndServiceOtherMember2023-01-012023-12-310001753162us-gaap:ProductAndServiceOtherMember2022-01-012022-12-3100017531622022-01-012022-12-310001753162us-gaap:CommonStockMember2022-12-310001753162us-gaap:AdditionalPaidInCapitalMember2022-12-310001753162us-gaap:RetainedEarningsMember2022-12-310001753162us-gaap:CommonStockMember2023-01-012023-12-310001753162us-gaap:AdditionalPaidInCapitalMember2023-01-012023-12-310001753162us-gaap:RetainedEarningsMember2023-01-012023-12-310001753162us-gaap:CommonStockMember2023-12-310001753162us-gaap:AdditionalPaidInCapitalMember2023-12-310001753162us-gaap:RetainedEarningsMember2023-12-310001753162us-gaap:CommonStockMember2021-12-310001753162us-gaap:AdditionalPaidInCapitalMember2021-12-310001753162us-gaap:RetainedEarningsMember2021-12-3100017531622021-12-310001753162us-gaap:CommonStockMember2022-01-012022-12-310001753162us-gaap:AdditionalPaidInCapitalMember2022-01-012022-12-310001753162us-gaap:RetainedEarningsMember2022-01-012022-12-310001753162us-gaap:VehiclesMember2023-12-310001753162srt:MinimumMemberus-gaap:ComputerEquipmentMember2023-12-310001753162srt:MaximumMemberus-gaap:ComputerEquipmentMember2023-12-310001753162us-gaap:FurnitureAndFixturesMember2023-12-310001753162us-gaap:TradeNamesMember2023-12-310001753162fthm:AgentRelationshipsMember2023-12-310001753162us-gaap:CustomerRelationshipsMember2023-12-310001753162fthm:KnowHowRelationshipsMember2023-12-310001753162us-gaap:ComputerSoftwareIntangibleAssetMember2023-12-31fthm:acquisition0001753162fthm:CornerstoneFinancialMember2022-01-242022-01-240001753162fthm:IproRealtyNetworkMember2022-02-082022-02-080001753162fthm:CornerstoneAndIProMember2022-02-080001753162fthm:CornerstoneAndIProMember2022-02-082022-12-310001753162fthm:RealEstateBrokerageMemberus-gaap:OperatingSegmentsMember2023-12-310001753162fthm:RealEstateBrokerageMemberus-gaap:OperatingSegmentsMember2022-12-310001753162fthm:MortgageSegmentMemberus-gaap:OperatingSegmentsMember2022-12-310001753162fthm:MortgageSegmentMemberus-gaap:OperatingSegmentsMember2023-12-310001753162fthm:TechnologyMemberus-gaap:OperatingSegmentsMember2022-12-310001753162fthm:TechnologyMemberus-gaap:OperatingSegmentsMember2023-12-310001753162us-gaap:CorporateNonSegmentMember2022-12-310001753162us-gaap:CorporateNonSegmentMember2023-12-310001753162us-gaap:ComputerEquipmentMember2023-12-310001753162us-gaap:ComputerEquipmentMember2022-12-310001753162us-gaap:FurnitureAndFixturesMember2022-12-310001753162us-gaap:LeaseholdImprovementsMember2023-12-310001753162us-gaap:LeaseholdImprovementsMember2022-12-310001753162fthm:KnowHowMember2023-12-310001753162us-gaap:TradeNamesMember2022-12-310001753162us-gaap:ComputerSoftwareIntangibleAssetMember2022-12-310001753162us-gaap:CustomerRelationshipsMember2022-12-310001753162fthm:AgentRelationshipsMember2022-12-310001753162fthm:KnowHowMember2022-12-310001753162us-gaap:ComputerSoftwareIntangibleAssetMember2023-01-012023-12-310001753162us-gaap:ComputerSoftwareIntangibleAssetMember2022-01-012022-12-310001753162srt:MaximumMemberus-gaap:SecuredOvernightFinancingRateSofrOvernightIndexSwapRateMemberfthm:MasterLoanAgreementMember2023-12-31xbrli:pure0001753162us-gaap:SecuredOvernightFinancingRateSofrOvernightIndexSwapRateMembersrt:MinimumMember2023-01-012023-12-310001753162fthm:WarehousingCreditAndSecurityAgreementMemberus-gaap:PrimeRateMember2023-12-310001753162fthm:WarehousingCreditAndSecurityAgreementMemberus-gaap:PrimeRateMember2022-12-310001753162fthm:MasterLoanAgreementMember2023-12-310001753162fthm:MasterLoanAgreementMember2022-12-310001753162fthm:MortgageParticipationPurchaseAgreementMember2023-12-310001753162fthm:MortgageParticipationPurchaseAgreementMember2022-12-310001753162fthm:MortgageParticipationPurchaseAgreementMember2023-09-300001753162fthm:WarehousingCreditAndSecurityAgreementMember2023-09-300001753162srt:MaximumMemberfthm:WarehousingCreditAndSecurityAgreementMemberus-gaap:SecuredOvernightFinancingRateSofrOvernightIndexSwapRateMember2023-12-310001753162fthm:WarehousingCreditAndSecurityAgreementMemberus-gaap:SecuredOvernightFinancingRateSofrOvernightIndexSwapRateMembersrt:MinimumMember2023-12-310001753162fthm:WarehousingCreditAndSecurityAgreementMember2023-12-310001753162fthm:A375SmallBusinessAdministrationInstallmentLoanDueMay2050Member2023-12-310001753162us-gaap:NotesPayableOtherPayablesMemberfthm:A375SmallBusinessAdministrationInstallmentLoanDueMay2050Member2023-12-310001753162us-gaap:NotesPayableOtherPayablesMemberfthm:A375SmallBusinessAdministrationInstallmentLoanDueMay2050Member2022-12-310001753162fthm:SeniorSecuredConvertiblePromissoryNoteMember2023-12-310001753162fthm:SeniorSecuredConvertiblePromissoryNoteMember2022-12-310001753162us-gaap:NotesPayableOtherPayablesMemberfthm:A60DirectorAndOfficerInsurancePolicyPromissoryNoteDueJuly312023Member2023-12-310001753162us-gaap:NotesPayableOtherPayablesMemberfthm:A60DirectorAndOfficerInsurancePolicyPromissoryNoteDueJuly312023Member2022-12-310001753162us-gaap:NotesPayableOtherPayablesMemberfthm:A90ExecutiveAndOfficerInsurancePolicyPromissoryNoteDueAugust12023Member2023-12-310001753162us-gaap:NotesPayableOtherPayablesMemberfthm:A90ExecutiveAndOfficerInsurancePolicyPromissoryNoteDueAugust12023Member2022-12-310001753162us-gaap:NotesPayableOtherPayablesMember2023-12-310001753162us-gaap:NotesPayableOtherPayablesMember2022-12-310001753162fthm:A60DirectorAndOfficerInsurancePolicyPromissoryNoteDueJuly312023Member2023-12-310001753162fthm:A60DirectorAndOfficerInsurancePolicyPromissoryNoteDueJuly312023Member2022-12-310001753162fthm:A90ExecutiveAndOfficerInsurancePolicyPromissoryNoteDueAugust12023Member2023-10-310001753162fthm:A90ExecutiveAndOfficerInsurancePolicyPromissoryNoteDueAugust12023Member2022-10-310001753162fthm:SeniorSecuredConvertiblePromissoryNoteMemberus-gaap:PrivatePlacementMember2023-04-130001753162fthm:SeniorSecuredConvertiblePromissoryNoteMemberus-gaap:PrivatePlacementMember2023-04-132023-04-130001753162fthm:SeniorSecuredConvertiblePromissoryNoteMemberus-gaap:SecuredOvernightFinancingRateSofrOvernightIndexSwapRateMemberus-gaap:PrivatePlacementMember2023-04-132023-04-130001753162fthm:SeniorSecuredConvertiblePromissoryNoteMembersrt:MinimumMemberus-gaap:PrivatePlacementMember2023-04-130001753162us-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel1Member2023-12-310001753162us-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel2Member2023-12-310001753162us-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel3Member2023-12-310001753162us-gaap:FairValueMeasurementsRecurringMember2023-12-310001753162us-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel1Member2022-12-310001753162us-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel2Member2022-12-310001753162us-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel3Member2022-12-310001753162us-gaap:FairValueMeasurementsRecurringMember2022-12-310001753162srt:MinimumMember2023-12-310001753162srt:MaximumMember2023-12-3100017531622022-03-1000017531622020-08-040001753162fthm:SecondaryPublicOfferingMemberus-gaap:CommonStockMember2023-01-012023-12-310001753162fthm:SecondaryPublicOfferingMemberus-gaap:CommonStockMember2023-12-310001753162fthm:StockPlan2017Member2023-12-310001753162fthm:OmnibusStockIncentivePlan2019Member2023-01-012023-12-310001753162fthm:OmnibusStockIncentivePlan2019Member2022-01-012022-12-310001753162fthm:OmnibusStockIncentivePlan2019Member2023-12-310001753162us-gaap:RestrictedStockMember2021-12-310001753162us-gaap:RestrictedStockMember2022-01-012022-12-310001753162us-gaap:RestrictedStockMember2022-12-310001753162us-gaap:RestrictedStockMember2023-01-012023-12-310001753162us-gaap:RestrictedStockMember2023-12-310001753162us-gaap:RestrictedStockUnitsRSUMember2021-12-310001753162us-gaap:RestrictedStockUnitsRSUMember2022-01-012022-12-310001753162us-gaap:RestrictedStockUnitsRSUMember2022-12-310001753162us-gaap:RestrictedStockUnitsRSUMember2023-01-012023-12-310001753162us-gaap:RestrictedStockUnitsRSUMember2023-12-3100017531622021-01-012021-12-310001753162us-gaap:EmployeeStockOptionMember2023-01-012023-12-310001753162fthm:CommissionAndOtherAgentRelatedCostMember2023-01-012023-12-310001753162fthm:CommissionAndOtherAgentRelatedCostMember2022-01-012022-12-310001753162fthm:OperationsAndSupportMember2023-01-012023-12-310001753162fthm:OperationsAndSupportMember2022-01-012022-12-310001753162fthm:TechnologyAndDevelopmentMember2023-01-012023-12-310001753162fthm:TechnologyAndDevelopmentMember2022-01-012022-12-310001753162us-gaap:GeneralAndAdministrativeExpenseMember2023-01-012023-12-310001753162us-gaap:GeneralAndAdministrativeExpenseMember2022-01-012022-12-310001753162fthm:MarketingMember2023-01-012023-12-310001753162fthm:MarketingMember2022-01-012022-12-310001753162us-gaap:RelatedPartyMember2023-01-012023-12-310001753162us-gaap:RelatedPartyMember2022-01-012022-12-310001753162us-gaap:EmployeeStockOptionMember2023-01-012023-12-310001753162us-gaap:EmployeeStockOptionMember2022-01-012022-12-310001753162us-gaap:RestrictedStockMember2023-01-012023-12-310001753162us-gaap:RestrictedStockMember2022-01-012022-12-310001753162us-gaap:RestrictedStockUnitsRSUMember2023-01-012023-12-310001753162us-gaap:WarrantMember2023-01-012023-12-310001753162us-gaap:WarrantMember2022-01-012022-12-310001753162us-gaap:DomesticCountryMember2023-01-012023-12-310001753162us-gaap:DomesticCountryMember2022-01-012022-12-310001753162us-gaap:StateAndLocalJurisdictionMember2023-01-012023-12-310001753162us-gaap:StateAndLocalJurisdictionMember2022-01-012022-12-310001753162us-gaap:DomesticCountryMember2023-12-31fthm:segment0001753162fthm:RealEstateBrokerageMemberus-gaap:OperatingSegmentsMember2023-01-012023-12-310001753162fthm:RealEstateBrokerageMemberus-gaap:OperatingSegmentsMember2022-01-012022-12-310001753162fthm:MortgageSegmentMemberus-gaap:OperatingSegmentsMember2023-01-012023-12-310001753162fthm:MortgageSegmentMemberus-gaap:OperatingSegmentsMember2022-01-012022-12-310001753162fthm:TechnologyMemberus-gaap:OperatingSegmentsMember2023-01-012023-12-310001753162fthm:TechnologyMemberus-gaap:OperatingSegmentsMember2022-01-012022-12-310001753162us-gaap:CorporateNonSegmentMember2023-01-012023-12-310001753162us-gaap:CorporateNonSegmentMember2022-01-012022-12-310001753162us-gaap:OperatingSegmentsMember2023-01-012023-12-310001753162us-gaap:OperatingSegmentsMember2022-01-012022-12-310001753162us-gaap:InvestorMember2023-12-3100017531622023-10-012023-12-310001753162fthm:MarcoFregenalMember2023-01-012023-12-310001753162fthm:MarcoFregenalMember2023-10-012023-12-310001753162fthm:MarcoFregenalMember2023-12-31

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

x ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended December 31, 2023

o TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

Commission file number 001-39412

FATHOM HOLDINGS INC.

(Exact name of registrant as specified in its charter)

| | | | | | | | |

| North Carolina | | 82-1518164 |

(State or other jurisdiction of incorporation or organization) | | (I.R.S. Employer Identification No.) |

2000 Regency Parkway Drive, Suite 300, Cary, North Carolina 27518

(Address of principal executive offices) (Zip Code)

(888) 455-6040

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Exchange Act:

| | | | | | | | | | | | | | |

| Title of Each Class | | Trading Symbol(s) | | Name of Each Exchange on Which Registered |

| Common Stock, No Par Value | | FTHM | | The NASDAQ Capital Market |

Securities registered pursuant to Section 12(g) of the Exchange Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes o No x

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Act.

Yes o No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. x Yes o No

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). x Yes o No

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| | | | | | | | | | | | | | | | | |

| Large accelerated filer | o | | Accelerated filer | | o |

| Non-accelerated filer | x | | Smaller reporting company | | x |

| | | Emerging growth company | | x |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. x

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act by the registered public accounting firm that prepared or issued its audit report. o

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements. o

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b). o

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes o No x

Based on the registrant’s closing price of $7.14 as quoted on the NASDAQ Capital Market on June 30, 2023, the aggregate market value of the registrant’s common stock held by non-affiliates of the registrant was approximately $66,327,887, Common stock held by each officer and director and by

each person known to the registrant who owned 10% or more of the outstanding common stock have been excluded in that such person may be deemed to be affiliates. This determination of affiliate status is not necessarily a conclusive determination for other purposes.

As of March 19, 2024, there were approximately 20,776,292 shares of the registrant’s common stock outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

The registrant intends to file a definitive proxy statement pursuant to Regulation 14A within 120 days after the end of the fiscal year ended December 31, 2023. Portions of such proxy statement are incorporated by reference into Part III of this Form 10-K.

Fathom Holdings Inc.

FORM 10-K

December 31, 2023

TABLE OF CONTENTS

NOTES

In this Annual Report on Form 10-K (this “Report”), and unless the context otherwise requires, “Fathom,” “we,” “us,” “our,” “the Company,” “our Company” and “our business” refer to Fathom Holdings Inc. and its direct and indirect subsidiaries as of December 31, 2023, taken as a whole.

We have a registered trademark with the United States Patent and Trademark Office (“USPTO”) for the name and logo of “intelliAgent” and “Fathom Realty”, as they relate to real estate and associated industries. All other trade names, trademarks and service marks appearing in this Report are the property of their respective owners. We have assumed that the reader understands that all such terms are source-indicating. Accordingly, such terms, when first mentioned in this Report, appear with the trade name, trademark or service mark notice and then throughout the remainder of this Report without trade name, trademark or service mark notices for convenience only and should not be construed as being used in a descriptive or generic sense.

SPECIAL NOTE REGARDING FORWARD-LOOKING STATEMENTS

This Report contains forward-looking statements that involve substantial risks and uncertainties. All statements, other than statements of historical facts, included in this Report regarding our strategy, future operations, future product research or development, future financial position, future revenues, projected costs, prospects, plans and objectives of management, are forward-looking statements. The words “anticipate,” “believe,” “goals,” “estimate,” “expect,” “intend,” “may,” “might,” “plan,” “predict,” “project,” “target,” “potential,” “will,” “would,” “could,” “should,” “continue,” “forecast” and similar expressions are intended to identify forward-looking statements, although not all forward-looking statements contain these identifying words. Forward-looking statements in this Report include, but are not limited to, statements about:

•the risks associated with government spending, inflation, the Federal Reserve’s policies and rate increases, and the unprecedented rapid increase in mortgage interest rates;

•our ability to remain an innovative leader in the real estate industry;

•whether we are able to effectively manage rapid growth in our business;

•the risks associated with litigation filed by or against us, and adverse results therefrom;

•our ability to prevent security breaches, cybersecurity incidents, and interruptions, delays and failures in our systems and operations;

•our ability to grow in the various local markets that we serve or expand into adjacent markets;

•whether we are successful in identifying and pursuing new business opportunities;

•our value proposition for agents, including giving them equity in our Company and allowing them to keep more of their commissions than traditional companies allow;

•our ability to ensure agents understand our value proposition so that we are able to attract, retain and incentivize agents;

•our ability to compete effectively with other companies in the real estate industry;

•the risks associated with making meaningful comparisons of successive quarters;

•our non-GAAP operating performance, as reported using Adjusted EBITDA, which is not equivalent to net income (loss) as determined under GAAP;

•our ability to protect the privacy of employees, independent contractors and consumers or the personal information they share with us so that we do not harm our reputation and business;

•our ability to expand, maintain and improve the systems and technologies upon which we rely on to operate;

•if we fail to maintain compliance with the law and regulations of federal, state, foreign, county governmental authorities, or private associations and governing boards;

•our ability to sell originated loans;

•our ability to obtain sufficient financing to fund the origination of mortgage loans and grow our mortgage business;

•our ability to establish and maintain effective internal controls over financial reporting;

•the risks associated with the loss of our current executive officers or other key management;

•our ability to protect intellectual property rights;

•our ability to evaluate potential vendors, suppliers and other business partners for acquisition to accelerate growth;

•our ability to integrate recently acquired businesses;

•our future revenues and growth prospects and our dependence on other contractors;

•our ability to obtain sufficient additional capital on reasonable terms to grow our business;

•our ability to manage technology that is currently being developed in foreign countries, including Brazil and India, and third-party off-shore service teams, including in the Philippines, which makes us subject to certain risks associated with foreign laws and regulations; and

•other forward-looking statements discussed elsewhere in this Report.

We might not achieve the plans, intentions or expectations disclosed in our forward-looking statements, and you should not place undue reliance on our forward-looking statements. Actual results or events could differ materially from the plans, intentions and expectations disclosed in the forward-looking statements we make. We have included important factors in the cautionary statements included in this Report, particularly in the section titled “Risk Factors” included in Item 1A of Part I of this Report, that we believe could cause actual results or events to differ materially from the forward-looking statements that we make. The environment in which we operate is highly competitive and rapidly changing and it is not possible for our management to predict all risks, as new risks emerge from time to time, such as the unprecedented increases in interest rates.

Except as required by law, we undertake no obligation to update or revise any forward-looking statements to reflect new information or future events or developments. You should therefore not rely on these forward-looking statements as representing our views as of any date subsequent to the date of this Report. You also should not assume that our silence over time means that actual events are bearing out as expressed or implied in such forward-looking statements.

SUMMARY OF RISK FACTORS

Our business is subject to significant risks and uncertainties that make an investment in us speculative and risky. Below we summarize what we believe are the principal risk factors, but these risks are not the only ones we face, and you should carefully review and consider the full discussion of our risk factors in the section titled “Risk Factors” included in Item 1A of Part I of this Report, together with the other information in this Report. If any of the following risks occurs (or if any of those listed elsewhere in this Report occur), our business, reputation, financial condition, results of operations, revenue, and future prospects could be seriously harmed.

Risks Related to Our Business

•If we do not remain an innovative leader in the real estate industry, we might not be able to grow our business and leverage our costs to achieve profitability;

•We might not be able to effectively manage rapid growth in our businesses;

•Industry, employee, or agent litigation and unfavorable publicity could negatively affect our future business;

•If we fail to grow in the various local markets that we serve or are unsuccessful in identifying and pursuing new business opportunities, our long-term prospects and profitability will be harmed;

•If agents do not understand our value proposition for them including allowing them to receive equity in our Company and keep more of their commissions than traditional real estate companies, we might not be able to attract, retain and incentivize agents or maintain our agent growth rate, which would adversely affect our revenue growth and results of operations;

•If we fail to expand effectively into adjacent markets, our growth prospects could be harmed;

•Adverse outcomes in litigation and regulatory actions against other companies and agents in our industry could adversely impact our financial results;

•We have a history of losses, and we might not be able to achieve or sustain profitability;

•Our revenue growth rates might not be indicative of our future growth, and we might not continue to grow at our recent pace, or at all;

•We currently use and intend to continue to use Adjusted EBITDA, a non-GAAP financial measure, in reporting our annual and quarterly results of operations; however, Adjusted EBITDA is not equivalent to net income (loss) from operations as determined under GAAP, and shareholders may consider GAAP measures to be more relevant to our operating performance;

•If we fail to protect the privacy of employees, independent contractors and consumers, or the personal information that they share with us, or if we fail to comply with privacy or data security legal requirements, our reputation and business could be significantly harmed;

•We participate in a highly competitive market, and pressure from other companies might adversely affect our business and operating results;

•Listing aggregator concentration and market power creates, and is expected to continue to create, disruption in the residential real estate brokerage industry, which might have a material adverse effect on our results of operations and financial condition;

•Our operating results are subject to seasonality and vary significantly across quarters during each calendar year, making meaningful comparisons of successive quarters difficult;

•Our business could be adversely affected if we are unable to expand, maintain and improve the systems and technologies upon which we rely to operate;

•Cybersecurity incidents, data breaches and other privacy/data security incidents could disrupt our business operations, and result in the loss or exposure of critical, confidential and/or sensitive information, which would adversely impact our reputation, result in costly regulatory investigations or litigation, create legal liability and harm our business;

•We face significant risk to our brands and revenue if we fail to maintain compliance with the law and regulations of federal, state, foreign, or county governmental authorities, or private associations and governing boards;

•Our mortgage business might be unable to sell its originated loans, in which case Fathom would need to service the loans and potentially foreclose on the home by itself or through a third party, either of which option could impose costs on Fathom. Our inability to sell originated loans could also expose us to adverse market conditions affecting mortgage loans;

•If we are unable to obtain sufficient financing through warehouse credit facilities to fund origination of mortgage loans, then we may be unable to grow our mortgage business;

•We might identify material weaknesses in the future that might cause us to fail to meet our reporting obligations or result in material misstatements of our financial statements. If we fail to remediate any material weaknesses or if we otherwise fail to establish and maintain effective internal controls over financial reporting, our ability to accurately and timely report our financial results could be adversely affected;

•We are an “emerging growth company,” and any decision on our part to comply only with certain reduced reporting and disclosure requirements applicable to emerging growth companies could make our common stock less attractive to investors;

•Loss of our current executive officers or other key management could significantly harm our business;

•Failure to protect intellectual property rights could adversely affect our business;

•We may evaluate potential vendors, suppliers and other business partners for acquisition to accelerate growth but might not succeed in identifying suitable candidates, or we may acquire businesses that negatively impact us;

•We have acquired businesses that are outside our core competencies as a real estate brokerage, which could be difficult to integrate, disrupt our core business, dilute stockholder value, and adversely affect our operating results and the value of our common stock;

•Our future revenue and growth prospects could be adversely affected by our dependence on other contractors, including off-shore contractors;

•We may require additional capital to support business growth, and this capital might not be available on acceptable terms, if at all;

•Part of our technology is currently being developed in foreign countries, including Brazil, which makes us subject to certain risks associated with foreign laws and regulations;

Risks Related to Our Industry

•Our results are tied to the residential real estate market, and we might be negatively impacted by downturns in this market and general global economic conditions;

•A lack of financing for homebuyers in the U.S. residential real estate market at favorable rates and on favorable terms could have a material adverse effect on our financial performance and results of operations;

•Potential reform of Fannie Mae or Freddie Mac or certain federal agencies or a reduction in U.S. government support for the housing market could have a material impact on our operations;

Risks Related to Ownership of Our Common Stock

•The requirements of being a public company may strain our resources, divert management’s attention, and affect our ability to attract and retain qualified board of director members;

•Our common stock price might fluctuate significantly, and the price of our common stock might be negatively impacted by factors which are unrelated to our operations;

•Our amended and restated bylaws provide that, unless we consent in writing, North Carolina state court is, to the fullest extent permitted by law, the sole and exclusive forum for substantially all disputes between us and our shareholders. This choice of forum provisions could limit the ability of shareholders to obtain a favorable judicial forum for disputes with us or our directors, officers or employees;

•Future sales of shares of our common stock by existing shareholders could depress the market price of our common stock;

•Joshua Harley, our Founder and former Chief Executive Officer, together with Marco Fregenal, our President and Chief Executive Officer and Chief Financial Officer, and a director, and Glenn Sampson, a significant shareholder, each own a significant percentage of our stock, and as a result, they can take actions that may be adverse to the interests of the other shareholders and the trading price for our common stock may be depressed; and

•If securities or industry analysts do not publish or cease publishing research or reports about us, our business or our market, or if they change their recommendations regarding our stock adversely, our stock price and trading volume could decline.

PART I

Item 1. Business.

Overview

Fathom Realty LLC was founded in January 2010 and later incorporated as Fathom Holdings Inc. in the state of North Carolina on May 5, 2017. We are a national, technology-driven, real estate services platform integrating residential brokerage, mortgage, title, insurance, and Software as a Service (“SaaS”) offerings to brokerages and agents by leveraging intelliAgent, our proprietary cloud-based software. The Company’s brands include Fathom Realty, Dagley Insurance, Encompass Lending, intelliAgent, LiveBy, Real Results, and Verus Title.

For Fathom Realty, our core business, our overhead business model leverages our proprietary software platform for management of real estate brokerage back-office functions, without the cost of physical brick and mortar offices or of redundant personnel. As a result, we can offer our agents significantly more of their commissions compared to traditional real estate brokerage firms; we do not split our agents’ commissions, but instead charge a flat fee per real estate transaction. We believe we offer our agents some of the best technology, training, and support available in the industry. We also offer our agents valuable benefits, including equity in our Company if they achieve growth goals. We believe our commission structure, business model, advanced technology offerings, and our focus on treating our agents well attract more agents and higher producing agents to join and stay with our Company.

Fathom Realty’s commission model is designed to empower real estate agents to build a more profitable business by allowing them to keep a high percentage of their commission without sacrificing support, technology, or training. We believe that by simply joining our company, agents from traditional model brokerages can increase their income by over 25% on average. More importantly, agents are able to take that increase and reinvest it into their marketing thereby increasing their number of transactions and revenue which also benefits Fathom.

Generally speaking, there are only two ways to make more money in real estate: increase revenue or decrease expenses. In a slowing housing market, it’s difficult to increase revenue. Our low flat transaction fee provides agents money to outspend their competition on marketing while netting the same amount of money as an agent at a traditional brokerage. With our low flat transaction fee, even during a decline in the housing market where home sales decline by 20%, we believe most real estate agents can net as much income as they did the year before at a traditional brokerage. In other words, they may close 20% fewer homes but could earn the same income as before under our fee model compared to being at a traditional brokerage. We believe this is a competitive advantage we can continue to leverage in our industry.

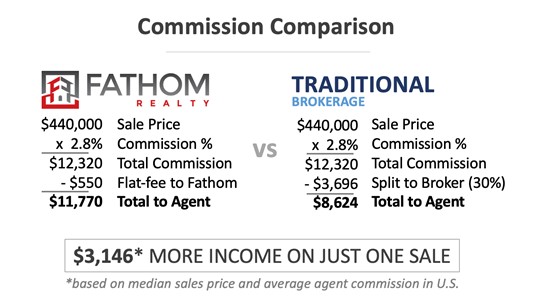

Traditional brokerage companies retain between 20% and 50% of the commission of their agents. Below is an example of a traditional brokerage company’s commission model assuming a 30% split, versus our commission model. This is an example of potential commission savings and results similar to the example below may vary and are not guaranteed.

We believe our commission model also allows agents to directly compete against discount brokerages and other disruptive new competitors. The flat transaction fee that we collect allows our agents to adjust the commission the charge accordingly to be highly competitive.

The commission we collect from our agents is our primary source of revenue. During 2022, from the gross commission income, we maintained a flat transaction fee of $500 per transaction and the remainder of any commission was retained by the agent. The $500 transaction fee was charged for each of the agent’s first 12 sales per agent’s anniversary year, and then $99 per sale for the rest of their anniversary year. For leases, we recognized revenue through lease commissions negotiated between our agents and landlords, and we retained $85 per transaction with the remainder paid to the agent.

Every agent also pays a $600 annual fee on their first sale (recognized as a reduction to Commission and other agent-related costs over the following twelve months), which helps cover our operating costs such as technology, errors and omissions insurance, training, and oversight.

In 2023, our agents paid $550 for each of their first 15 completed sales transactions, up from $500 on their first 12 sales transactions. For each sales transaction after the first 15, our agents will pay $150 for the rest of their anniversary year, up from $99 in 2022. We have also discontinued our agent stock grant program effective December 31, 2022, which had provided for our agents to receive $200 in stock grants for every five transactions completed. We currently plan to continue to provide stock grants to agents based on metrics achieved for recruiting new agents. In 2023, our average cost to recruit a new agent was $1,050 and our annual cost associated with each agent was $1,150 so we break even in an agent’s first year if he or she completes just two sales.

Starting in January 2024, there will be an increase of the agent’s annual fee which is charged on an agent’s first transaction of each anniversary year from $600 to $700. A second change includes a new fee which affects sales of properties over $600,000 and will be in addition to the agent’s transaction fee of $550. This new ‘High-Value Property Fee’ will consist of an additional $200 on properties priced between $600,000 and $999,999. Then, there will be an additional fee of $250 charged for each $500,000 tier range over a $1,000,000 property price. The Company expects these changes could add an estimated $3.1 million in EBITDA for the year ended December 31, 2024. (See our Current Report on Form 8K filed with the SEC on November 28, 2023 for further information).

In just fourteen years since we launched our Company, we have grown rapidly with operations in 40 states plus the District of Columbia. We achieved gross commission income of approximately $325.4 million on $13.3 billion in real estate sales volume for the year ended December 31, 2023. As of December 31, 2023, we had approximately 11,795 licensed agents or brokers working for us.

In March 2023, we were ranked the #6 largest independent real estate brokerage firm and the #10 overall largest brokerage firm in the United States (per available data). These rankings were published by The Real Trends Five Hundred based on several criteria including transaction size, sales volume, affiliation, top movers, core services, and others. Fathom also was listed in the top three of the Top 100 Places to Work in Dallas Fort Worth, five years in a row by the Dallas Morning News.

In February 2022, the Company completed its acquisition of iPro Realty Network (“iPro”). The acquisition of iPro, a real estate brokerage business, has helped us to expand our reach in the Utah real estate market.

Also in February 2022, the Company completed its acquisition of Cornerstone Financial (“Cornerstone”). The acquisition of Cornerstone, a real estate mortgage business, has helped us to expand our reach in the DC and surrounding markets.

Industry Background

We primarily operate in the U.S. residential real estate industry, with a market size of over $2.5 trillion with over 4.8 million new and existing properties sold in the United States in 2023. Our agents also opportunistically engage in commercial real estate transactions. We derive most of our revenues from serving buyers and sellers of existing homes. According to the National Association of Realtors, or the NAR, existing home sales represent approximately 90% of the overall market by number of transactions.

The U.S. residential real estate industry has a long history of growth, despite periodical downturns. Period downturns, like the current one, can often be defined by things over which the industry has no control, such as economic uncertainty and increased interest rates. (see "Industry Trends" for further detail below). The following information is based on data published by the NAR. This data includes the significant and lengthy downturn from the second half of 2005 through 2011, and in that time frame, the number of annual U.S. existing home sale transactions declined by approximately 39%. Beginning in 2012, the U.S. residential real estate industry began its recovery, and the number of annual U.S. existing home sale units improved. However, there was another housing downturn beginning in 2022, when severe inflation gave rise to high interest rates which caused U.S. existing home sale transactions to decline by approximately 33.5% in 2023, according to Realtor.com.

Industry Trends

In addition to the negative impacts of recent economic uncertainty and increased interest rates, we believe the following trends have impacted the U.S. real estate market and that their impact will continue to accelerate:

•according to the NAR, 97% of homebuyers use the Internet to search for homes, illustrating the importance of technology and transition away from expensive brick-and-mortar offices in the industry, while only 2% found their agent through the agent’s office;

•nevertheless, according to the NAR, 89% of home buyers and 89% of home sellers still used an agent or broker in 2023, up from 86% for both buyers and sellers in 2022, for various reasons, including the relative size, importance and infrequency of a home sale for any individual;

•the complexity of the home selling or buying process continues to require the best personal service possible, while technology can make the process and business more efficient; and

•downturns like the current one are inevitable, and favor companies with lower cost business models that also pay agents higher commissions.

Our Strategy

Our goal is to be the leading 100% commission real estate brokerages in the United States while offering superior customer service, state of the art technology, and a great company culture. We have grown rapidly since inception, and plan to accelerate our growth through the following aspects of our vision:

•offer full brokerage services via our technology-enabled, low-overhead business model;

•attract and retain high-producing agents by offering high compensation per transaction and industry-leading benefits;

•use our publicly traded stock to further incentivize agents;

•continue to enhance and develop our proprietary software platform to facilitate our own business and potentially increase our revenue by licensing it to others; and

•pursue further growth through potential acquisitions, including potentially using our publicly traded stock as consideration, depending on its value at the time.

Technology

Fathom Realty operates primarily as a cloud-based real estate brokerage by utilizing our proprietary consumer-facing website, https://www.FathomRealty.com, and our internal proprietary technology, intelliAgent(R), to manage our brokerage operations. Through our website, we provide buyers, sellers, landlords, and tenants with access to all available properties for sale or lease on the multiple listing service, or MLS, in each of the markets in which we operate. We provide each of our agents their own personal website that they can modify to match their personal branding. Our website also gives consumers access to our network of professional real estate agents and vendors. Through a combination of our proprietary technology platform and several third-party systems, we provide our agents with marketing, training, and other support

services, as well as client and transaction management. Our technology, services, data, lead generation, and marketing tools are designed to be used by our agents to represent their real estate clients with best-in-class service.

Internally, we use our technology to provide agents with opportunities to increase their profitability, reduce risk, and develop professionally, while fostering a culture that values collaboration, strength of community, and commitment to serving the consumer’s best interests. We provide our agents with the systems, support, professional development and infrastructure designed to help them succeed in unpredictable, and often challenging, economic conditions. This includes delivering 24/7 access to collaborative tools and training for real estate agents.

Specifically, using advanced Internet-based software, we can improve compliance and oversight while providing, at no cost to our agents, technology tools and services to our agents and their customers, including:

•a robust, mobile-friendly, customer-facing corporate website providing access to view all homes for sale and lease in the markets that we serve, with the ability to search and save favorite properties and receive alerts for new properties that fit their criteria;

•a customizable, mobile-friendly agent website with home search, lead capture, and blogging capabilities;

•an advanced customer relationship management system, with visitor tracking, property alerts, and customer communication, all designed to help convert leads into customers;

•social media tools to enhance agent marketing and visibility;

•streamlined solicitation, collection, verification and posting of customer testimonials;

•single property websites for our agents’ listings;

•a wide array of on-demand training modules for the professional development of agents at all levels of experience; and

•agent access to intelliAgent(R), which is described in more detail below.

Our proprietary intelliAgent(R) real estate technology platform provides a suite of brokerage and agent level tools, technology, business processes, business intelligence and reporting, training. IntelliAgent includes, but is not limited to consumer facing websites, transaction management, personnel management, customer relationship management, accounting management for agent transactions, reporting, social media marketing and other marketing and marketing repository, along with a future marketplace for add-on services and third-party technology. Our intelliAgent rollout strategy began with the core technology needed by every real estate brokerage to manage its agents, its agents’ transactions, commission structures, payments, and compliance, as well as the ability to gain a better understanding of the operations of the business through business intelligence and robust reporting. IntelliAgent has since grown to include brokerage and agent-level websites, content creation and management, customer relationship management, social media marketing, agent reviews, a training platform, and marketing repository. Our technology roadmap includes our own fully-integrated e-signature platform, goal setting and accountability for agents, expense tracking for agents, and APIs for integration with additional third-party tools. We intend for intelliAgent to be more than just a technology platform for Fathom; we might someday use a simplified version of intelliAgent as a platform to unify independent brokerages through a smarter broker network, which would help them effectively compete against larger regional and national brands. This should allow us to monetize a portion of our technology and generate revenue from small-to-medium sized brokerages and agents who would not otherwise join our company. We believe that intelliAgent also provides us with the platform to more fully integrate our mortgage, title, and insurance companies that are part of Fathom Holdings. This deeper integration is designed to encourage a higher level of agent adoption and use of our various services companies and therefore create a better agent experience, customer experience, and generate higher revenues for our company and add value for our shareholders.

In addition to building intelliAgent internally, in March 2021 we acquired Naberly, a home search website and customer relationship management technology company, to help us achieve technology independence, which further enhanced our proprietary intelliAgent platform to give us a stronger competitive advantage. Naberly allowed us to further improve our operational efficiency while reducing costs from third party providers. Offering even more robust technology to help our agents grow their businesses is a key strategy to continuing our solid agent growth trajectory. In the future, we

also intend to roll out an enhanced version of the Naberly platform to launch a national real estate portal to help generate leads for our Fathom agents, as well as non-Fathom agents, in the markets in which we are not currently operating.

To develop and accelerate the growth of agents joining Fathom, we developed the Fathom Talent Acquisition Platform. The Fathom Talent Acquisition Platform combines talented agents, technology and process. Fathom has built an extensive database of potential agents who we believe would fit the Fathom culture and benefit from joining the Company. A content marketing strategy updates candidates on the latest developments and offers that may be of interest to them in growing their business. Additionally, a team of experienced recruiters focuses on personally introducing and sharing the Fathom brands value proposition with real estate professionals across the country. The team works within a customer relationship management system to nurture longer term opportunities, and help recruit agents who want to join our team of independent contractors. These elements are designed to build brand awareness and position Fathom as the brokerage of choice for agents making career decisions.

Our Focus on Agents

We believe that agents deliver unique value to the specific customers they serve in different ways depending upon the knowledge, skills or expertise of the agent and the needs and desires of the customers. We also believe that customers who choose agents because of the agent’s skills and service prioritize the agent's skill service levels and style over the brokerage brand with which the agent is affiliated. Therefore, we heavily emphasize serving our agents, so that we attract and retain the best in the industry.

In a recent study by the NAR, only 3% of home sellers chose their agent because of the agent's brokerage. We believe home buyers and sellers choose an agent because of the agent's marketing prowess, professionalism, and personality. To capitalize on this, we focus on helping our agents improve professionally and increase their financial ability to invest in their personal marketing.

Cost Structure

The lower overall cost of operating our business primarily virtually enables us to offer our agents a 100% commission model. We charge each agent a flat fee per real estate transaction. Consequently, this higher commission retained by our agents combined with our unique delivery of support services and the flexibility it provides for agents has facilitated our growth over the past several years. We also differentiate ourselves by not charging our agents royalties or franchise fees. A commission calculator on our website allows agents to determine how much money they could make if they join our company.

We believe we offer agents further opportunity to increase their overall revenue and income, because they can invest the additional income earned under our fee structure in incremental marketing.

Our Markets

Currently, our market is the United States. We currently operate in 40 states plus the District of Columbia:

| | | | | | | | | | | | | | |

| Alabama | | Kentucky | | Ohio |

| | | | |

| Arizona | | Louisiana | | Oklahoma |

| | | | |

| Arkansas | | Maryland | | Oregon |

| | | | |

| California | | Massachusetts | | Rhode Island |

| | | | |

| Colorado | | Michigan | | Pennsylvania |

| | | | |

| Delaware | | Minnesota | | South Carolina |

| | | | |

| Florida | | Missouri | | Tennessee |

| | | | |

| Georgia | | Montana | | Utah |

| | | | |

| Hawaii | | Nebraska | | Virginia |

| | | | |

| Idaho | | Nevada | | Washington |

| | | | |

| Illinois | | New Hampshire | | West Virginia |

| | | | |

| Iowa | | New Jersey | | Wisconsin |

| | | | |

| Indiana | | New Mexico | | Washington D.C. |

| | | | |

| Kansas | | North Carolina | | |

We primarily target urban or suburban areas or regions with populations of at least 50,000, of which there are approximately 775 in the United States. We believe this provides us opportunity for continued growth. We have expanded rapidly since our inception fourteen years ago. As we continue to expand, we might also target smaller rural markets as well as move into Canada.

Competition

The residential real estate brokerage industry is highly competitive with low barriers to entry for new participants. We believe that recruitment and retention of independent sales agents and independent sales agent teams are critical to the business and financial results of a brokerage. Competition for independent sales agents in our industry is high and has intensified particularly for the more productive independent sales agents. Competition for independent sales agents is generally subject to numerous factors, including remuneration and benefits, other expenses borne by independent sales agents, leads or business opportunities generated for the independent sales agent from the brokerage, independent sales agents’ perception of the value of the broker’s brand affiliation, marketing and advertising efforts by the brokerage or franchisor, technology, continuing professional education, and other services provided by the brokerage or franchisor.

We compete with three major categories of competitors:

•national independent real estate brokerages, franchisees of national and regional real estate franchisors, regional independent real estate brokerages, and discount and limited-service brokerages;

•companies that employ technologies intended to disrupt the traditional brokerage model or eliminate agents from, or minimize the role they play in, the home sale transaction, such as through the reduction of brokerage commissions; and

•other non-traditional models that operate outside of the brokerage industry, such as companies that purchase homes directly from sellers.

Many of our competitors are much larger than us, with more capital to fund growth and survive downturns like the current one, and many of them have greater brand awareness. Some of our competitors are also increasingly well-funded, which strengthens their competitive position and ability to offer aggressive compensation arrangements to top-performing sales agents. Moreover, a growing number of companies are competing in non-traditional ways for a portion of the gross commission income generated by home sale transactions. For example, listing aggregators and other web-based real estate service providers not only compete with our business by establishing relationships with independent sales agents and/or buyers and sellers of homes, they also increasingly charge brokerages and independent sales agents for advertising on their sites.

Our ability to successfully compete is important to our prospects for growth. Our ability to compete may be affected by the recruitment, retention and performance of independent sales agents, the location of offices and target markets, the services provided to independent sales agents, the fees charged to independent sales agents, the number and nature of competing offices in the vicinity, affiliation with a recognized brand name, community reputation, technology and other factors. Our success may also be affected by national, regional and local economic conditions.

Intellectual Property

We have a registered trademark with the USPTO for the name and logo of “intelliAgent” and “Fathom Realty”, as they relate to real estate and associated industries. We also own the rights to the domain names FathomHoldings.com, FathomRealty.com, FathomCareers.com, intelliAgent.com, Naberly.com, and LiveBy.com.

We have developed and own the intelliAgent software. We also license lesser third-party software, but none of which we believe is critical to our ability to compete or operate effectively. While we currently utilize these vendors to provide our services in the short-term, we believe other alternatives are available in the longer term, should they be needed, to license or develop replacement technology. Our March 2021 acquisition of Naberly was intended to reduce our need for third party software.

If necessary, we will aggressively assert our rights under trade secret, unfair competition, trademark and copyright laws to protect our intellectual property. We protect these rights through trademark law, the maintenance of trade secrets, the development of trade dress, and, where appropriate, litigation against those who are, in our opinion, infringing these rights.

While an assertion of our rights could result in a substantial cost and diversion of management effort, we believe the protection and defense against infringement of our intellectual property rights are essential to our business. There is also risk that someone else will claim that we are violating their intellectual property rights, which could cost money and time to defend, even if we are successful.

Seasonality of Business

Seasons and weather traditionally impact the real estate industry. Continuous poor weather or natural disasters negatively impact listings and sales. Spring and summer seasons historically reflect greater sales periods in comparison to fall and winter seasons. The latter periods also tend to see greater agent attrition. We have historically experienced lower revenues during the fall and winter seasons, as well as during periods of unseasonable weather, which reduces our operating income, net income, operating margins and cash flow.

Real estate listings precede sales and a period of poor listing activity will negatively impact revenue. Past performance in similar seasons or during similar weather events can provide no assurance of future or current performance, and macroeconomic shifts in the markets we serve can conceal the impact of poor weather and/or seasonality.

Home sales in successive quarters can fluctuate widely due to a wide variety of factors, including holidays, national or international emergencies, the school year calendar’s impact on timing of family relocations, interest rate changes, speculation of pending interest rate changes and the overall macroeconomic market. Our revenue and operating margins each quarter will remain subject to seasonal fluctuations, poor weather, natural disasters and macroeconomic market changes that may make it difficult to compare or analyze our financial performance effectively across successive quarters.

Furthermore, the residential real estate market and the real estate industry in general are often cyclical, characterized by protracted periods of depressed home values, lower buyer demand, inflated rates of foreclosure and often changing regulatory or underwriting standards applicable to mortgages. The best example of this was the significant downturn in the U.S. residential real estate market between 2005 and 2011. Such depressed real estate cycles are often followed by extended periods of higher buyer demand, lower available real estate supply and increasing home values. While we believe we are well-positioned to compete during a downturn, our business is affected by these cycles in the residential real estate market, which can make it difficult to compare or analyze our financial performance effectively across successive periods.

Government Regulation

We serve the residential real estate industry which is regulated by federal, state and local authorities as well as private associations or state sponsored associations or organizations. We are required to comply with federal, state, and local laws, as well as private governing bodies’ regulations, which, when combined, result in a highly-regulated industry.

We are also subject to federal and state regulations relating to employment, contractor, and compensation practices. Except for our employed state agents, all agents in our brokerage operations have been retained as independent contractors, either directly or indirectly through third-party entities formed by these independent contractors for their business purposes. With respect to these independent contractors, like most brokerage firms, we are subject to the Internal Revenue Service regulations and applicable state law guidelines regarding independent contractor classification. These regulations and guidelines are subject to judicial and agency interpretation.

Real Estate Regulation - Federal

The Real Estate Settlement Procedures Act of 1974, as amended, or RESPA, became effective on June 20, 1975. RESPA requires lenders, mortgage agents, or servicers of home loans to provide borrowers with pertinent and timely disclosures regarding the nature and costs of the real estate settlement process. RESPA also protects borrowers against certain abusive practices, such as kickbacks, and places limitations upon the use of escrow accounts. RESPA also requires detailed disclosures concerning the transfer, sale, or assignment of mortgage servicing, as well as disclosures for mortgage escrow accounts.

The Dodd-Frank Wall Street Reform and Consumer Protection Act, or the Dodd-Frank Act, moved authority to administer RESPA from the Department of Housing and Urban Development to the new Consumer Financial Protection Bureau, or the CFPB. The CFPB released a five-year strategic plan in February 2018 indicating that it intends to continue to focus on protecting consumer rights while engaging in rulemaking to address unwarranted regulatory burdens. As a result, the regulatory framework of RESPA applicable to our business may be subject to change. The Dodd-Frank Act also increased regulation of the mortgage industry, including: (i) generally prohibiting lenders from making residential mortgage loans unless a good faith determination is made of a borrower’s creditworthiness based on verified and documented information; (ii) requiring the CFPB to enact regulations to help assure that consumers are provided with timely and understandable information about residential mortgage loans that protect them against unfair, deceptive and abusive practices; and (iii) requiring federal regulators to establish minimum national underwriting guidelines for residential mortgages that lenders will be allowed to securitize without retaining any of the loans’ default risk. In addition, federal fair housing laws generally make it illegal to discriminate against protected classes of individuals in housing or brokerage services. Other federal laws and regulations applicable to our business include (i) the Federal Truth in Lending Act of 1969; (ii) the Federal Equal Credit Opportunity; (iii) the Federal Fair Credit Reporting Act; (iv) the Fair Housing Act; (v) the Home Mortgage Disclosure Act; (vi) the Gramm-Leach-Bliley Act; (vii) the Consumer Financial Protection Act; (viii) the Fair and Accurate Credit Transactions Act; and (ix) the Do Not Call/Do Not Fax Act and other federal and state laws pertaining to the privacy rights of consumers, which affects our opportunities to solicit new clients.

Real Estate Regulation - State and Local Level

Real estate and brokerage licensing laws and requirements vary by state. In general, all individuals and entities lawfully conducting businesses as real estate agents or sales associates must be licensed in the state in which they carry on business and must at all times be in compliance.

States require a real estate broker to be employed by the brokerage firm or permit an independent contractor classification, and the broker may work for another broker conducting business on behalf of the sponsoring broker.

States may require a person licensed as a real estate agent, sales associate or salesperson to be affiliated with a broker in order to engage in licensed real estate brokerage activities or allow the agent, sales associate or salesperson to work for another agent, sales associate or salesperson conducting business on behalf of the sponsoring agent, sales associate or salesperson. Agents, sales associates or salespersons are generally classified as independent contractors; however, real estate firms can also offer employment.

Engaging in the real estate brokerage business requires obtaining a real estate broker license (although in some states the licenses are personal to individual agents). In order to obtain this license, most jurisdictions require that a member or manager be licensed individually as a real estate broker in that jurisdiction. If applicable, this member or manager is responsible for supervising the entity’s licensees and real estate brokerage activities within the state.

Real estate licensees, whether they are salespersons, individuals, agents or entities, must follow the state’s real estate licensing laws and regulations. These laws and regulations generally specify minimum duties and obligations of these licensees to their clients and the public, as well as standards for the conduct of business, including contract and disclosure requirements, record keeping requirements, requirements for local offices, escrow trust fund management, agency representation, advertising regulations and fair housing requirements.

In each of the states where we have operations, we assign appropriate personnel to manage and comply with applicable laws and regulations.

Most states have local regulations (city or county government) that govern the conduct of the real estate brokerage business. Local regulations generally require additional disclosures by the parties to a real estate transaction or their agents, or the receipt of reports or certifications, often from the local governmental authority, prior to the closing or settlement of a real estate transaction as well as prescribed review and approval periods for documentation and broker conditions for review and approval.

Third-Party Rules

Beyond federal, state and local governmental regulations, the real estate industry is subject to rules established by private real estate groups and/or trade organizations, including, among others, state Associations of REALTORS ® (AOR), and local Associations of REALTORS ® (AOR), the National Association of Realtors ® (NAR), and local Multiple Listing Services (MLSs). “REALTOR” and “REALTORS” are registered trademarks of the National Association of REALTORS(R).

Each third-party organization generally has prescribed policies, bylaws, codes of ethics or conduct, and fees and rules governing the actions of members in dealings with other members, clients and the public, as well as how the third-party organization’s brand and services may or might not be deployed or displayed.

Human Capital

As of December 31, 2023, we had 241 full-time employees.

Our operations are overseen directly by management. Our management oversees all responsibilities in the areas of corporate administration, training, agent relations, business development, technology, and research. We intend to expand and retain our current management and skilled employees with experience relevant to our businesses.

As of December 31, 2023, we had approximately 11,795 licensed agents and brokers whom we classify as independent contractors.

None of our employees or agents are represented by unions, and we believe our employee and agent relations are good.

Information about our Executive Officers

The following table sets forth current information concerning our executive officers:

| | | | | | | | | | | | | | |

| Name | | Age | | Position |

| Marco Fregenal | | 60 | | Chief Executive Officer, President and Chief Financial Officer |

| | | | |

| Samantha Giuggio | | 54 | | Chief Operations Officer of Fathom Realty |

Marco Fregenal – President and Chief Executive Officer, Director

Marco Fregenal has been our Chief Executive Officer since November, 2023, and our Chief Financial Officer since 2012. He has also served as our President since January 1, 2018. Prior to this, Mr. Fregenal served as our Chief Operating Officer and Chief Financial Officer from May 1, 2012 to December 31, 2017. Prior to joining our company, Mr. Fregenal served as Chief Operating Officer and Chief Financial Officer of EvoApp Inc., a provider of social media business intelligence, from 2009 to 2012. He was also the Chief Executive Officer and Chief Financial officer of Carpio Solutions, an information technology solutions company, from 2007 to 2009. Mr. Fregenal received a B.S. in economics from Rutgers University and a Masters in Econometrics and Operations Research from Monmouth University.

Samantha Giuggio — Chief Broker Operations Officer

Samantha Giuggio has served as our Chief Operations Officer for Fathom Realty since June 2019. Prior to this, she served as Senior Vice President from October 2015 to June 2019. From April 2014 to October 2015, Ms. Giuggio served as our Regional Vice President and Vice President of Operations. She also served as our District Director RDU from February 2013 to April 2014. She served as an Agent and Group Leader Training Coordinator with us prior to this. Ms. Giuggio received an associate’s degree in hospitality management from Holyoke Community College.

Fourth Quarter 2023 Executive Officer Changes

On November 10, 2023, Joshua Harley, the Chief Executive Officer, Director and Chairman of the Board of Directors of Fathom Holdings, Inc. (the "Board") resigned from his role as CEO and Director of the Company, effective November 13, 2023. On November 10, 2023, the Board appointed Marco Fregenal, President and Chief Financial Officer of the Company, to serve as Chief Executive Officer, in addition to his current responsibilities, and appointed Scott Flanders, current Director, as Chair of the Board, both effective as of November 13, 2023. For further information, please see the Company's current report on Form 8-K filed on November 10, 2023.

A search for a new Chief Financial Officer began in early 2024.

Other Information

We make available, free of charge through our website, our annual report on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K and all amendments to those reports as soon as is reasonably practicable after such material is electronically filed with or furnished to the Securities and Exchange Commission (“SEC”) pursuant to Section 13(a) or 15(d) of the Securities Exchange Act of 1934, as amended (the “Exchange Act”). The SEC maintains an Internet site that contains these reports at www.sec.gov.

Our corporate website address is www.fathominc.com. The information contained in, or that can be accessed through, our website is not part of this Report.

Item 1A. Risk Factors.

An investment in our securities involves a high degree of risk. You should consider carefully the risks and uncertainties described below together with the other information included in this Report, including our consolidated financial statements and the related notes thereto included elsewhere in this Report. The occurrence of any of the following risks may materially and adversely affect our business, financial condition, results of operations, cash flows, reputation and future prospects. In this event, the market price of our common stock could decline, and you could lose part or all of your investment.

Risks Related to Our Business

If we do not remain an innovative leader in the real estate industry, we might not be able to grow our business and leverage our costs to achieve profitability.

Innovation has been critical to our ability to compete for clients and real estate agents. If competitors follow our practices or develop more innovative practices, our ability to achieve profitability may diminish or erode. For example, other brokerages could develop or license cloud-based office platforms that are equal to or superior to ours. If we do not remain on the forefront of innovation, we might not be able to achieve or sustain profitability, particularly in the current environment of economic uncertainty and increased interest rates, which are having a negative effect on the real estate industry.

The market for Internet products and services is characterized by rapid technological developments, evolving industry standards and customer demands, and frequent new product introductions and enhancements. Our future success will depend in significant part on our ability to continually improve the performance, features and reliability of our technological developments in response to both evolving demands of the marketplace and competitive product offerings, and there can be no assurance that we will be successful in doing so.

We might not be able to effectively manage rapid growth in our business.

We might not be able to scale our business services and support quickly enough to meet the growing needs of our real estate agents. If we are not able to grow efficiently, our operating results could be harmed. As we continue to add new agents and make acquisitions, we will need to devote additional financial and human resources to improving our internal systems, integrating with third-party systems, and maintaining infrastructure performance. In addition, we will need to appropriately scale our internal business systems and our services organization, including support of our affiliated agents as our demographics expand over time. Any failure of, or delay in, these efforts could impair system performance and negatively impact our agents' satisfaction. These issues could result in difficulty in both attracting and retaining agents. Even if we can upgrade our systems and expand our staff, such expansion may be expensive, complex, and place increasing demands on our management. We could also face inefficiencies or operational failures as a result of our efforts to scale our infrastructure and we might not be successful in maintaining adequate financial and operating systems and controls as we expand. Moreover, there are inherent risks associated with upgrading, improving and expanding our information technology systems. We cannot be sure that the expansion and improvements to our infrastructure and systems will be fully or effectively implemented on a timely basis, if at all. These efforts may reduce revenue and our margins and adversely impact our financial results.

Continued technological and geographic growth could also strain our ability to maintain reliable service levels for our users and advertisers, develop and improve our operational, financial, and management controls, enhance our reporting systems and procedures, and recruit, train, and retain highly skilled personnel. Our products are accessed by many users, often simultaneously. If the use of our marketplace continues to expand, we might not be able to scale our technology to accommodate increased capacity requirements, which might result in interruptions or delays in service. The failure of our systems and operations to meet our capacity requirements could result in interruptions or delays in service or impede our ability to scale our operations.

These issues could result in difficulty in both attracting and retaining agents. Even if we are able to upgrade our systems and expand our staff, such expansion may be expensive, complex, and place increasing demands on our management. We could also face inefficiencies or operational failures as a result of our efforts to scale our infrastructure and we might not be successful in maintaining adequate financial and operating systems and controls as we expand. Moreover, there are inherent risks associated with upgrading, improving and expanding our information technology systems. We cannot be sure that the expansion and improvements to our infrastructure and systems will be fully or effectively implemented on a timely basis, if at all. These efforts may reduce revenue and our margins and adversely impact our financial results.

If we fail to grow in the various local markets that we serve or are unsuccessful in identifying and pursuing new business opportunities our long-term prospects and profitability will be harmed.

To capture and retain market share in the various local markets that we serve, we must compete successfully against other brokerages for agents and for the consumer relationships that they bring. Our competitors could lower the fees that they charge to agents or could raise the compensation structure for those agents. Our competitors may have access to

greater financial resources than us, allowing them to undertake expensive local advertising or marketing efforts. In addition, our competitors may be able to leverage local relationships, referral sources, and strong local brand and name recognition that we have not established. Our competitors could, as a result, have greater leverage in attracting both new and established agents in the market and in generating business among local consumers. Our ability to grow in the local markets that we serve will depend on our ability to compete with these local brokerages.

If we don't grow organically in local markets, or if we fail to successfully identify and pursue new business opportunities we may decide to change our business model and operations to improve revenue. Such changes may disproportionately increase our expenses or reduce profit margins. For example, we may allocate resources to acquire lower margin brokerage models or to develop a commercial real estate division. These decisions could involve significant up-front costs that may only be recovered after long periods of time. In addition, any of these additional activities could expose us to additional compliance obligations and regulatory risks.

If we fail to continue to grow in the local markets we serve or if we fail to successfully identify and pursue new business opportunities, our long-term prospects, financial condition and results of operations may be harmed, and our stock price may decline.

Our value proposition for agents includes allowing them to keep more of their commissions than traditional companies do, and receive equity in our Company, which is not typical in the real estate industry. If agents do not understand our value proposition, we might not be able to attract, retain and incentivize agents or maintain our agent growth rate, which would adversely affect our revenue growth and results of operations.

Participation in our commission plan represents a key component of our agent and broker value proposition. Agents might not understand or appreciate our value. In addition, agents might not appreciate other components of our value proposition including the systems and tools that we provide to agents, and the professional development opportunities we create and deliver. We compete with many other real estate brokerages for qualified agents and if agents do not understand the elements of our agent value proposition, or do not perceive it to be more valuable than the models used by most competitors, we might not be able to attract, retain and incentivize new and existing agents to grow our revenue. This could also negatively impact our agent growth rate. Our net licensed agent and broker base grew by approximately 14% from 10,370 licensed agents and brokers at December 31, 2022, to 11,795 licensed agents and brokers at December 31, 2023. Because we derive revenue from real estate transactions in which our agents receive commissions, increases in our licensed agent base correlate to increases in revenue. A slowdown in our licensed agent growth rate would have a material adverse effect on revenue growth and could adversely affect our results of operations.

If we fail to expand effectively into adjacent markets, our growth prospects could be harmed.